François Watier and Philip Lambrinos Recognized Among TopGun Investment Minds 2026

Since “Liberation Day” in April 2025, U.S. Small Cap equities have staged a decisive comeback, with the Russell 2000 returning 25.72% versus 17.80% for the S&P 500 over the twelve months to March 2026. This white paper argues that the current environment, characterized by elevated volatility, mean reversion, and wide valuation dispersion, creates an exceptional opportunity for active managers. Our strategy has historically offered long-term alpha, a superior risk/reward profile, and a portfolio currently trading at an approximate 20% discount to intrinsic value.

Following several years of underperformance relative to large caps, U.S. Small Cap equities have entered a new phase. Since “Liberation Day” in April 2025, the Russell 2000 has delivered a gross return of 25.72% compared with 17.80% for the large-cap benchmark over the twelve months to March 2026. This significant reversal reflects improving fundamentals and greater relative valuation attractiveness for small caps. While the pronounced sentiment-driven, low-quality market environment in the past year proved to be highly adversarial for active small-cap managers, with a significant majority of active strategies underperforming their benchmark in the last twelve months, we believe that a very compelling case in favor of active management, and of strategies such as ours, has developed.

This paper sets out the four primary reasons why institutional allocators should consider rotating from passive to active management in U.S. Small Cap equities at this juncture.

Historically, persistent alpha generation has been more achievable in U.S. Small Cap than in highly efficient large-cap markets, where passive investing tends to dominate. The informational inefficiency inherent to smaller companies, limited analyst coverage, lower liquidity, and greater fundamental dispersion, creates a fertile environment for bottom-up stock selection.

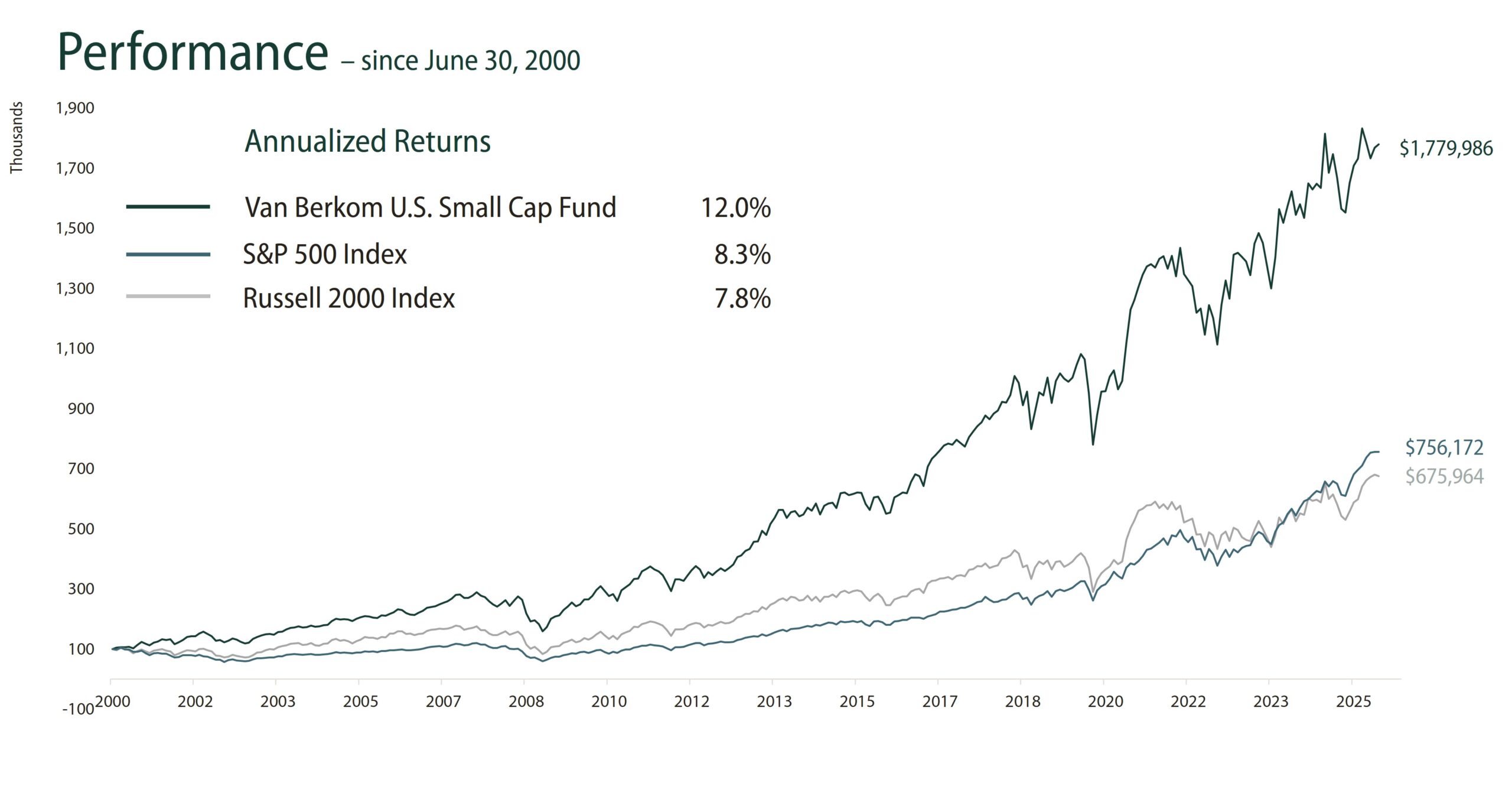

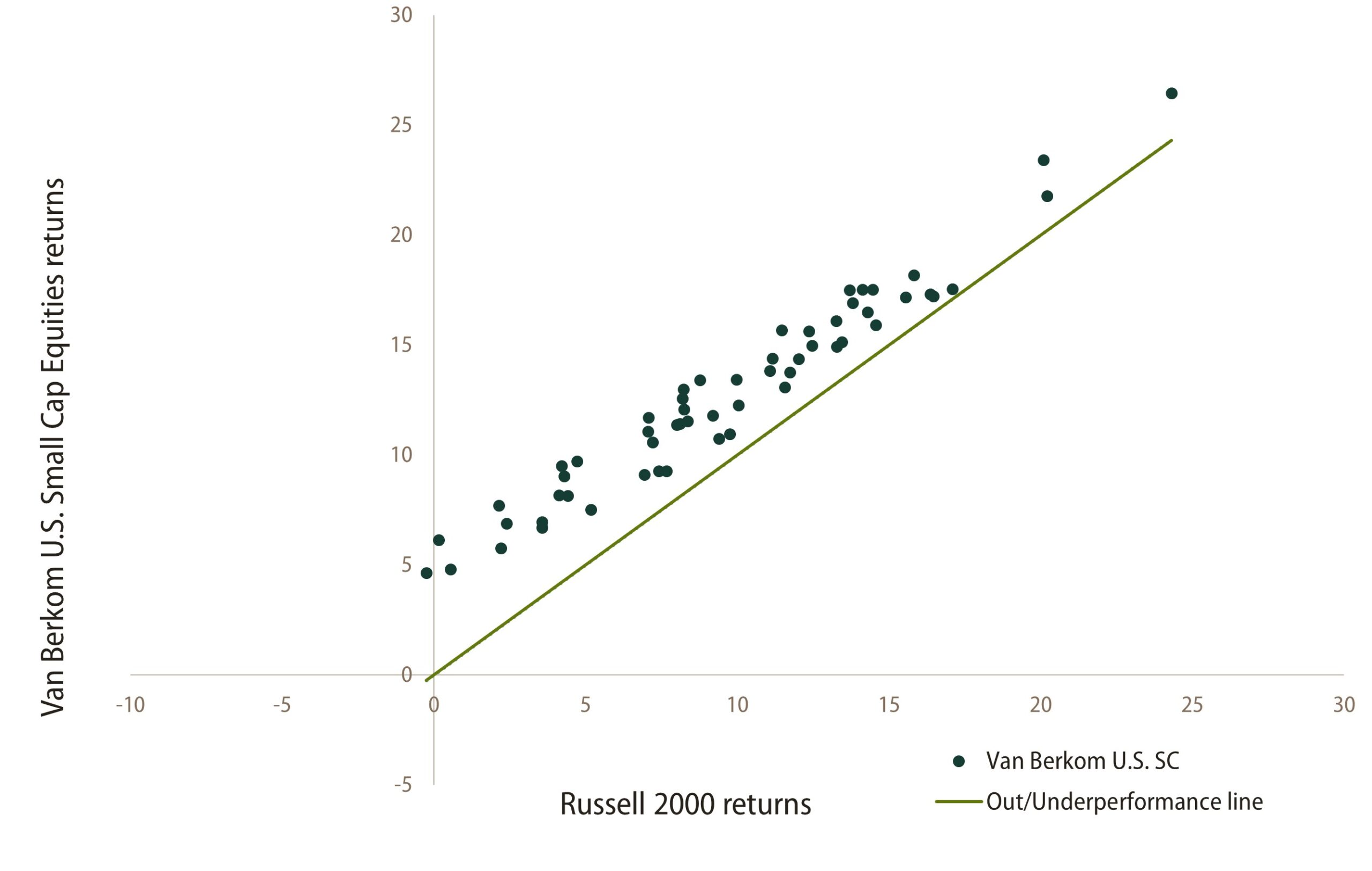

Our track record substantiates this thesis. Since inception, our first, and still active, client in the U.S. Small Cap strategy has generated a significant cumulative alpha premium relative to both the Russell 2000 and the S&P 500. Rolling five-year analysis confirms that Van Berkom’s U.S. Small Cap strategy has outperformed its benchmark over all five-year periods as measured at the end of each quarter since current leadership took over in early 2007.

Key Data Point

Our strategy has outperformed the Russell 2000 benchmark in every rolling five-year period since 2007.

Quarterly Observations

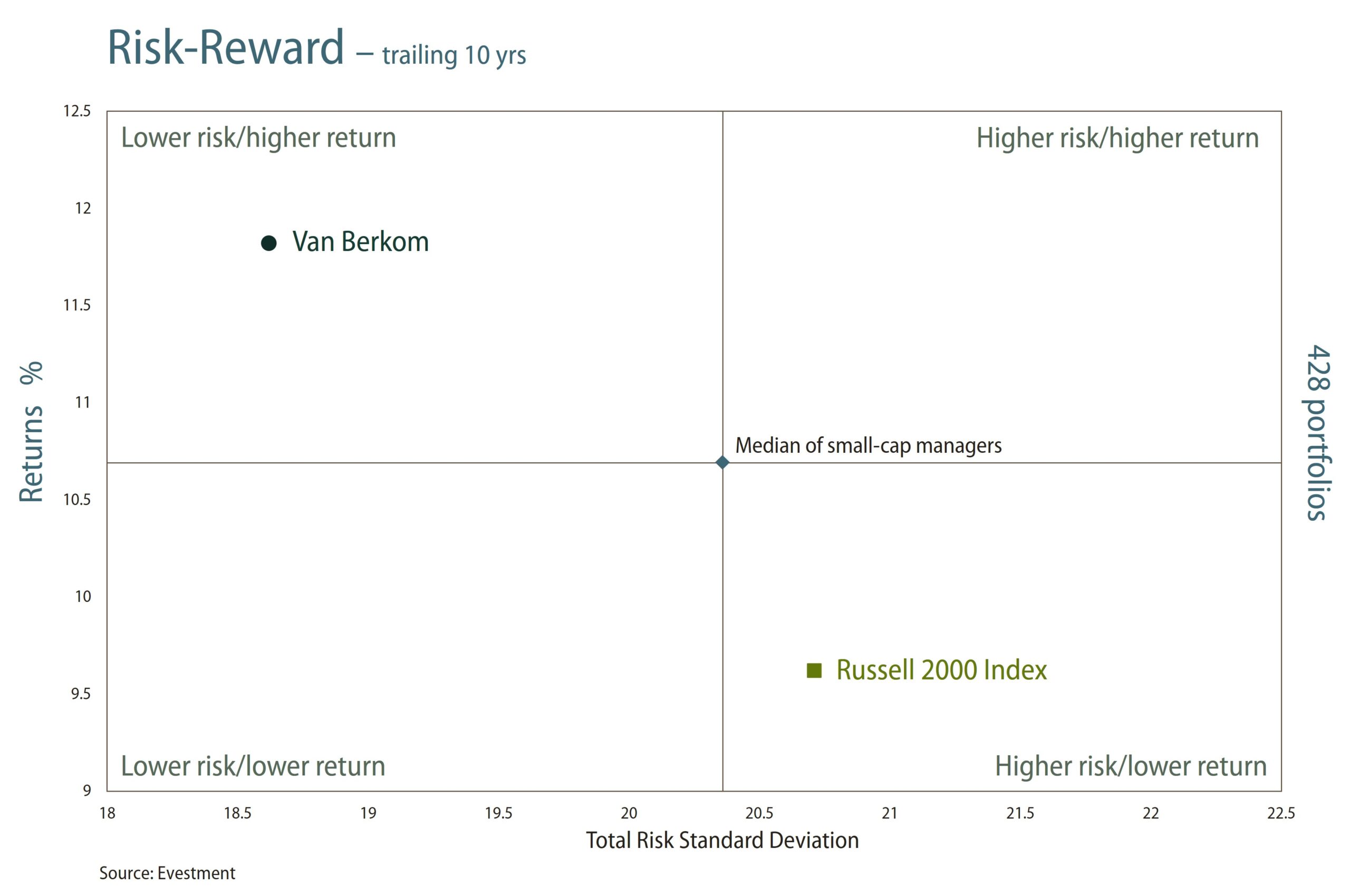

Active management has the potential to deliver a superior risk/reward profile compared with passive exposure. Over long-term periods such as the last ten years, our strategy has consistently generated higher annualized returns than the Russell 2000 while exhibiting lower realized volatility, carrying a much lower risk profile than its benchmark.

This combination of higher returns and reduced volatility is particularly compelling for all types of institutional investors,

as it aligns with the need for capital preservation, balance-sheet stability, and efficient risk management

over the long term.

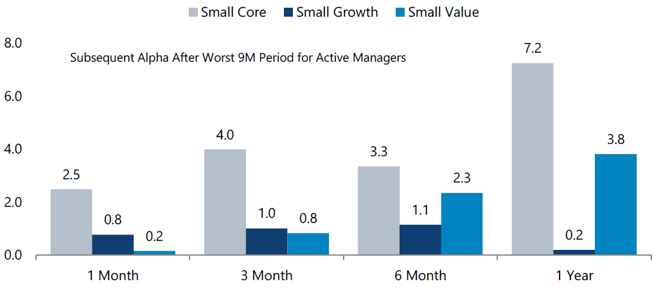

Market history consistently demonstrates that the worst periods for active U.S. Small Cap managers are often followed by some of the strongest alpha-generation environments. Periods of market stress and macro-driven price dislocation, precisely the conditions observed since mid-2024, tend to suppress active returns temporarily before catalyzing significant outperformance.

The current environment, characterized by elevated geopolitical uncertainty, interest-rate volatility, and wide fundamental dispersion, bears strong resemblance to prior inflection points. After an extended period characterized by a pronounced low-quality, sentiment-driven and momentum-led market environment that has been largely detached from company-specific fundamentals, asset allocators who rotate into active management at such junctures have historically been rewarded with outsized absolute and relative long-term returns.

Sources: FactSet; Lipper Analytical Services; FTSE Russell; Jefferies

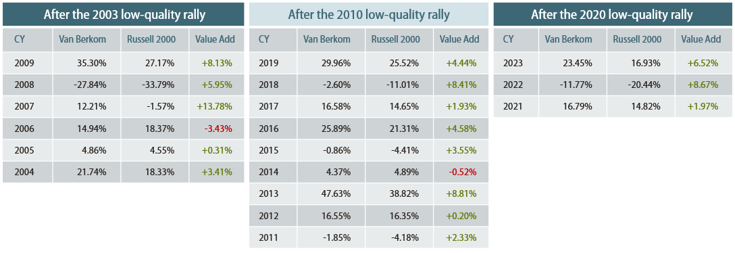

This is the fourth low-quality market environment that we have experienced over the 25+ year history of our U.S. Small Cap strategy. If investors go back and look at the prior three occurrences (2003, 2010 and 2020) where we faced such low-quality market environments that were disconnected from company-specific fundamentals, they will find that our U.S. Small Cap strategy significantly outperformed its small-cap benchmark over the subsequent years after such prior low-quality rallies.

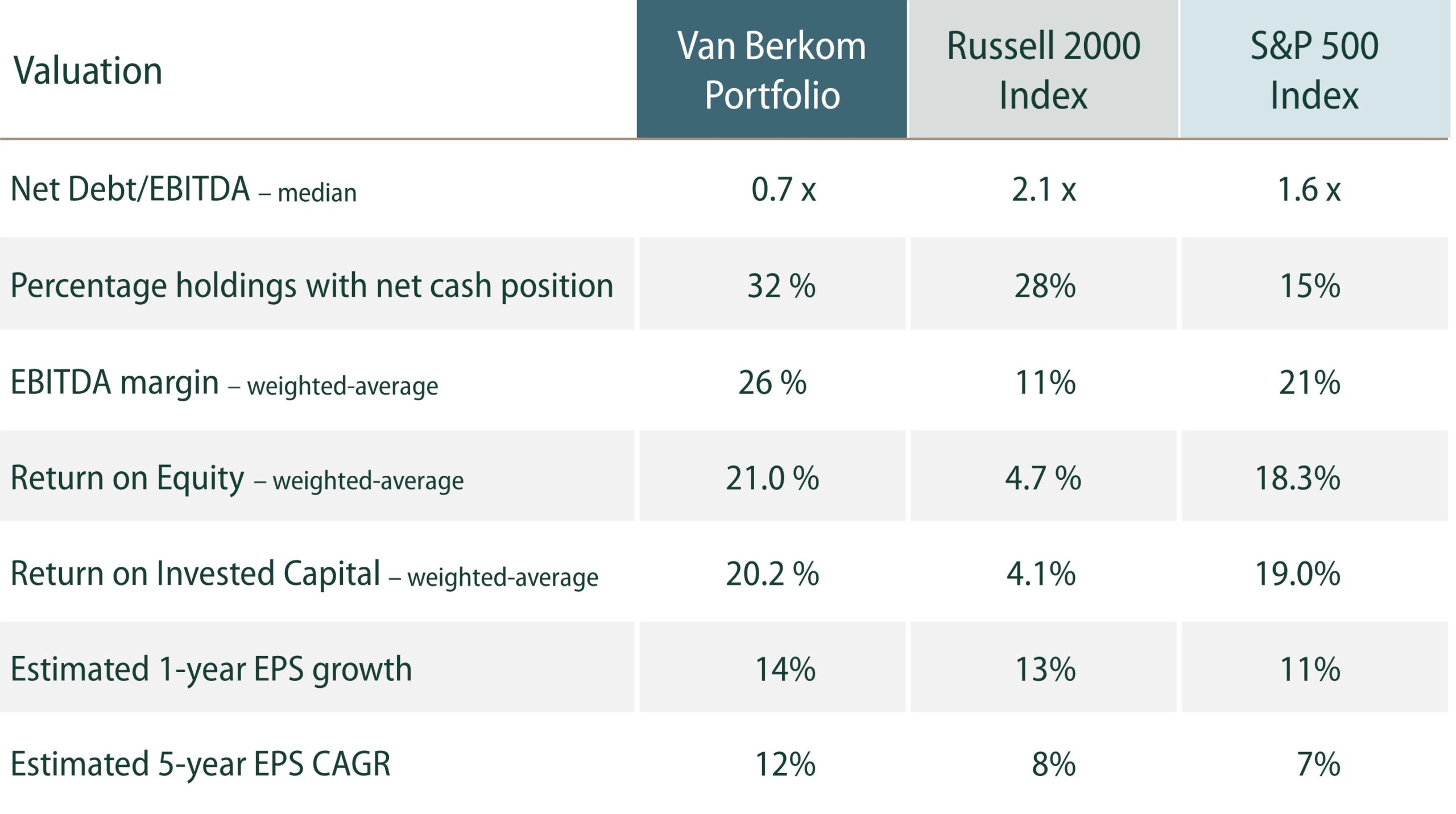

Van Berkom’s U.S. Small Cap portfolio is positioned as a high-quality, capital-efficient growth strategy, rather than a traditional benchmark-hugging exposure. As of March 31, 2026, the portfolio compares favorably to both the Russell 2000 and S&P 500 across all key fundamental dimensions:

Given the really high and superior ROE and ROIC ratios of our portfolio companies and their structurally faster earnings and cash flow growth profiles through cycles which have consistently been in the 10%–15% range annually over the past 25 years, we believe that the stocks of these businesses are capable of compounding value at approximately 10%–15% per year over a five-year horizon, a rate roughly consistent with a near double in the invested capital of our clients over five-year periods.

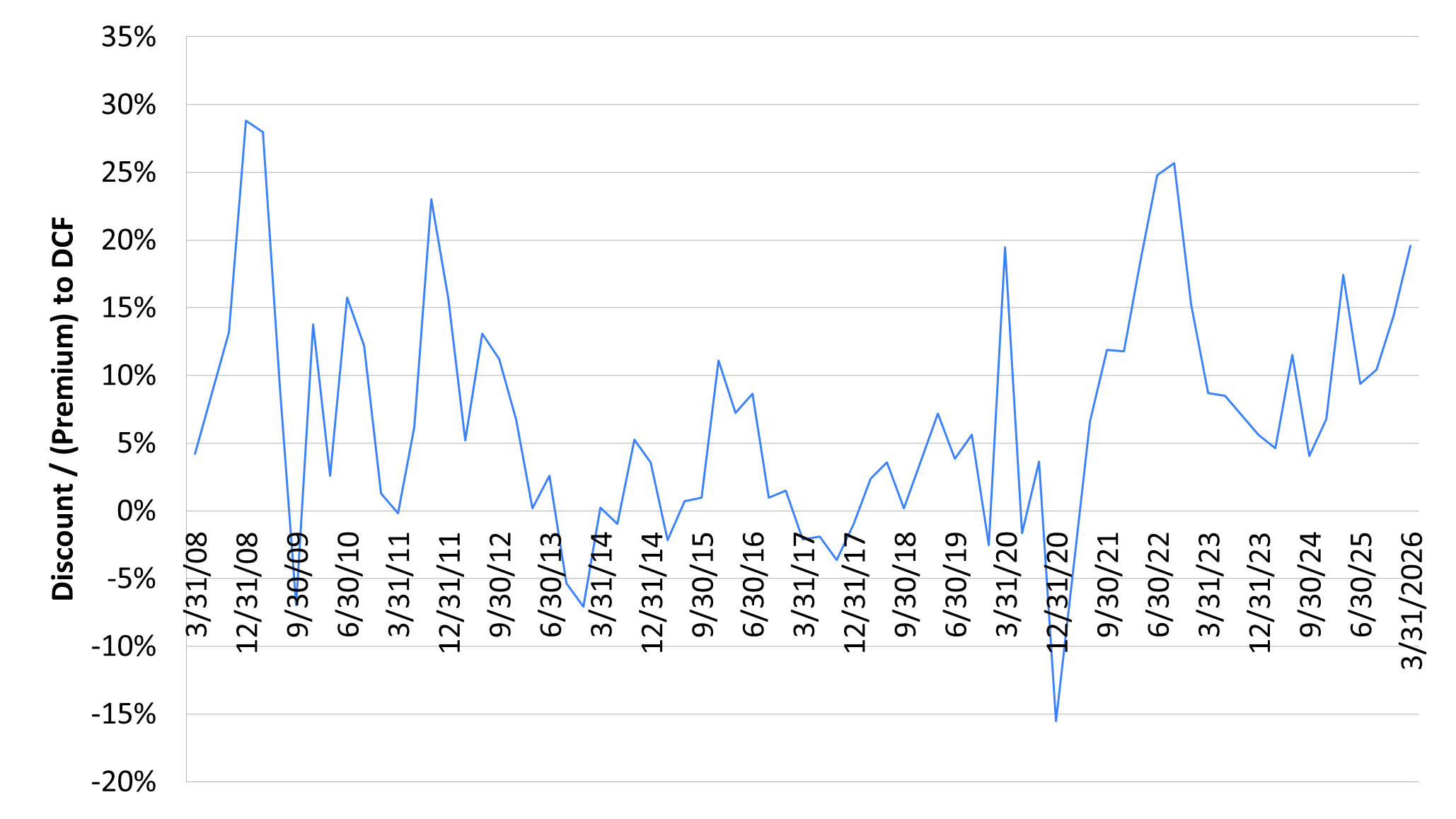

We estimate that our small-cap strategy is currently trading at an approximate 20% discount to intrinsic value based on our conservative valuation framework. Over the past 20 years, comparable valuation levels have been observed only during 2008–2009, 2011, and the 2022 rate-hike-driven bear market. Despite continued double-digit earnings growth across our portfolio companies, market prices have declined year-to-date, resulting in unusually attractive valuation multiples and a compelling setup for potential strong future returns.

Current Opportunity

Portfolio trading at ~20% discount to intrinsic value, a level last seen in 2008–2009, 2011, and 2022.

Historical Discount/(Premium) to Intrinsic Value for Van Berkom’s U.S. Small-Cap strategy (based on our extensive DCF methodology and analysis)

The convergence of four factors, a proven long-term alpha track record, a superior risk/reward profile, favourable mean-reversion dynamics, and an unprecedented valuation discount, makes the current moment an especially compelling entry point for active U.S. Small Cap management.

Passive exposure to the Russell 2000 captures the average, including the weakest companies in the index. Active management, applied with discipline and rigor, enables allocators to own only the highest-quality businesses at the most attractive prices, precisely the approach that has driven our long-term outperformance.

We invite you to discuss how the Van Berkom U.S. Small Cap strategy can complement your existing portfolio and help capture the significant opportunity we see in this asset class.

For more information, you can contact Andy Kong, Partner, Head of Global Business Development

at akong@vanberkomglobal.com.

Disclosures

This page has been prepared by Van Berkom & Associates (“Van Berkom”) for informational purposes only and is intended solely for the use of institutional investors. Van Berkom, also known and operating as Van Berkom Global Asset Management, is a Canadian firm federally incorporated and registered as portfolio manager and as exempt market dealer with the Autorité des marchés financiers of Quebec and with the securities commissions of the nine other Canadian provinces, and as investment fund manager, where required. Van Berkom is also registered with the U.S. Securities and Exchange Commission as an independent investment adviser. Past performance is not indicative of future results. All figures are in USD and as of December 31, 2025, unless otherwise stated. Performance is calculated gross of fees and withholding taxes and is annualized for periods longer than 12 months. The information contained herein is believed to be reliable but is not guaranteed as to its accuracy or completeness. This document does not constitute investment advice or an offer or solicitation to buy or sell any security.

We put our passion and expertise at your service.